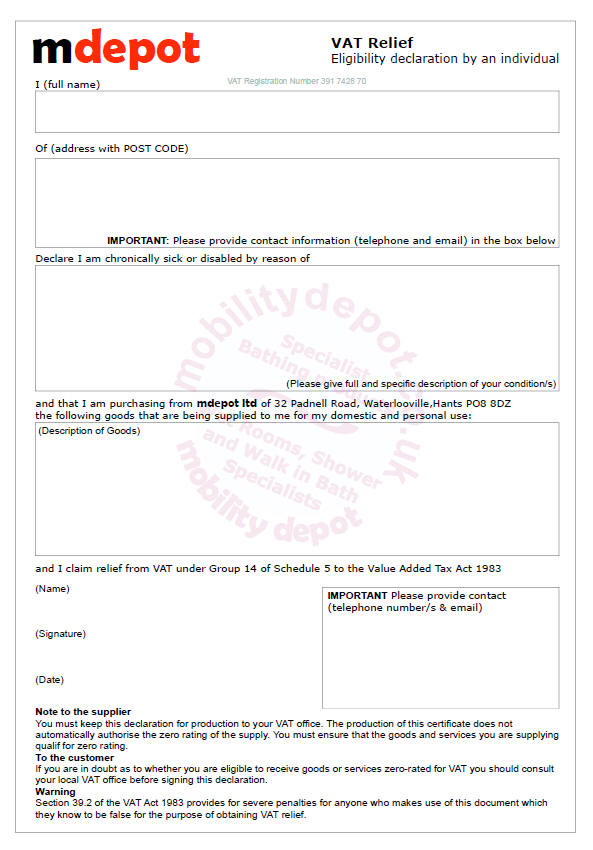

The essence of regulations

permitting VAT Relief

Only products that are manufactured specifically for or

adapted for use by disabled persons are eligible for exemption from Value Added Tax (VAT).

These are known as 'Qualifying Goods'.

To obtain exemption from VAT on your eligible

purchase you must also qualify as an individual.

Broadly speaking, if you

are disabled or suffer from a chronic condition that causes severe difficulty

with movement you may qualify. (These notes are only intended as a guide and

do not constitute a definitive statement. Please check with HMRC)

Note: Present guidelines tend to

preclude persons who

'are waiting for an operation'

or who

'suffer from a

condition that will improve in the short term after treatment'.

The rules are at

best vague. The relief is intended to assist persons with long term chronic

conditions. A letter from a Doctor, medical practitioner or such like can often

strengthen your case. But remember, the form upon which you will make your claim

is a 'self declaration' and as such you take full responsibility for the claim.

If you qualify you may be able to recover some or

all of the VAT you pay on qualifying products.

Important:

Do not take eligibility for granted.

H.M. Revenue and Customs will seek to recover

unpaid V.A.T. if it is subsequently

discovered your claim is erroneous.

Severe penalties exist for V.A.T. evasion.

Do not attempt to obtain exemption fraudulently. If you are unsure - seek

guidance.

VAT relief is only available if...

You (a qualifying person) purchase

a product that qualifies - i.e. a product which has been manufactured or adapted for use by a

disabled person, for your own use.

Relief is not available if...

-

you are a contractor purchasing for a project

or installation for a disabled person (you however may be expected to offer

your customer exemption on any works carried out for them provided they and

the works qualify).

-

if you

are disabled and purchasing a product considered to be ordinary (i.e goods

generally available that have not been designed for or modified for use by a

disabled person - an ordinary saucepan for example)

-

if you are disabled and wish to

purchase a product for somebody else to use. You may not claim Relief if

your purchase is a gift for example.

|